Savings Tips

- Save your loose change. Putting aside fifty cents a day over the course of a year will allow you to save nearly 40% of a $500 emergency fund.

- Keep track of your spending. At least once a month, use credit card, checking, and other records to review what you've purchased. Then, ask yourself if it makes sense to reallocate some of this spending to an emergency savings account.

- Never purchase expensive items on impulse. Think over each expensive purchase for at least 24 hours. Acting on this principle will mean you have far fewer regrets about impulse purchases, and far more money for emergency savings.

- Use debit and credit cards prudently. To minimize interest charges, try to limit credit card purchases to those you can pay off in full at the end of the month. If you use a debit card, don't rely on an overdraft feature to spend money you don't have. With either approach, you'll have more money available for emergency savings.

- Are you looking for an effective way to establish a budget? Beginning on the first day of a new month, get a receipt for everything you purchase. Stack and review receipts at the end of the month, and you will clearly be able to see where your money is going.

- It pays to practice preventative dental care, since a good cleaning routine helps prevent fillings, root canals, and dental crowns, which are expensive and no fun.

- Most people don’t track what they spend and may not realize when expenses add up to more than their budget can handle. To keep track of what you spend, trying putting away what you think you will spend for the month on transportation, food, entertainment, etc., into envelopes. This may help you avoid buying things you don’t need necessarily need, and what’s left over put automatically into saving.

- Take advantage of military discounts, always ask, all they can do is say they don't offer a discount. Plan out trips in advance and check with your local installation Information, Travel and Tickets office to see if they offer discount tickets. And don’t forget the best deal of all – investing in your Thrift Savings Plan. Find more information for retirement savings for your spouse or family member: Save for Retirement.

- One way to establish a savings discipline is to “save” an amount equal to whatever is spent on nonessential indulgences. Put a matching amount in a cookie jar for expenditures for beer, wine, cigarettes, designer coffee, etc. If you can’t afford to save the matching amount, you can’t afford the $4 super almond low-fat latte.

- Take the amount the item costs and divide it into your hourly wage. If it’s a $50 pair of shoes and you make about $10 an hour, ask yourself, are those shoes really worth five long hours of work? It helps keep things in perspective.

- Aim for short-term savings goals, such as setting aside $20 a week or month rather than long term savings goals, such as $200 over a year. People save more successfully when they keep the short-term goal in sight.

- Save money by utilizing the Commissary and Exchange. The overall yearly savings of shopping at the Commissary on discounted items and tax-free at the Exchange can really add up!

- Substitute coffee for expensive coffee drinks.The $2 a day you could well save by buying a coffee rather than a cappuccino or latte would allow you, over the course of a year, to completely fund a $500 emergency fund.

- Bring lunch to work. If buying lunch at work costs $5, but making lunch at home costs only $2.50, then in a year, you could afford to create a $500 emergency fund and still have money left over.

- Eat out one fewer time each month. If it costs you $25 to eat out, but only $5 to eat in, then the $20 you save each month allows you to almost completely fund a $500 emergency savings account.

- Shop for food with a list and stick to it. People who do food shopping with a list, and buy little else, spend much less money than those who decide what to buy when they get to the food market.The annual savings could easily be hundreds of dollars.

- Avoid overdrawing your checking account- ever! Overdraft fees can send you into a spiral of debt each month. The $20-30 you could save with each purchase that overdraws your account each month would save you enough money to nearly fully fund a $500 emergency savings account.

- Reduce credit card debt by $1,000. That $1,000 debt reduction will probably save you $150-200 a year, and much more if you're paying penalty rates of 20-30%.

- Make your monthly credit card payment on time. The $30-35 you save by not being charged a late fee each month on one card would save you most of the money you need for $500 in emergency savings

- Use only the ATMs of your bank or credit union. Using the ATM of another financial institution once a week could well cost you $3 a withdrawal, or more than $150 over the course of a year.

- Shop around for auto and homeowners' insurance: Before renewing your existing policies each year, check out the rates of competing companies (see the website of your state insurance department). Their annual premiums may well be several hundred dollars lower.

- Raise the deductibles on auto and homeowners' insurance: Being willing to pay $500-1,000 on a claim, rather than only $100-250, can reduce annual premiums by as much as several hundred dollars. (Just make sure your emergency can fully cover these deductibles, plus other possible occurrences surrounding an insurance claim)

- Assess your need for life insurance coverage. If your children are now on their own, or if your spouse works, you may not need as much life insurance protection. The annual premiums on a term life policy would typically fully fund an emergency savings account.

- Consider dropping credit insurance coverage on installment loans. Many consumers don't need credit insurance because they have sufficient assets to protect themselves in the event of death, disability, or unemployment. Terminating this coverage often reduces financing costs by three percentage points, a savings of about $1,000 on a four-year $20,000 installment loan.

- Keep your car engine tuned and its tires inflated to their proper pressure. Doing both can save you up to $100 a year in gas.

- Shop around for gas. Comparing prices at different stations and using the lowest-octane (recommended by the car owner's manual) can save you hundreds of dollars a year.

- When driving, avoid fast start-ups and stops. Over time, you will save hundreds of dollars on lower gas and maintenance costs.

- Take fewer cab rides. Using public transit instead of cabs can save you $5-10 per trip or more. If you're a frequent cab user, the savings could completely fund your emergency savings account.

- Check all airlines for cheap fares. Since no website lists all discount carriers, also check out the websites of discount carriers like Southwest and Jet Blue, possibly saving you hundreds of dollars.

- Don't pay for space you don't need. Americans have relatively large houses and apartments. Think about more efficiently using space so you can purchase or rent less square footage.

- Live relatively near your workplace. While this isn't always possible, driving 5,000 miles less a year can lower transportation costs by more than $1,000.

- Refinance your mortgage to lower interest charges. Consider refinancing your mortgage to lower the rate and/or term. On a 15-year fixed-rate mortgage, for about every $100,000 you finance, lowering your interest rate by 1% or more can save you more than $9,000 in interest charges over the life of the loan. On a 30-year fixed rate mortgage, for every $100,000 financed, the savings is even bigger with a 1% drop in your interest rate you could save over $21,000 over the term of your loan. Changing your term alone with a $100,000 30-year mortgage to a 15-year will save you over $50,000 in interest charges. And, you will accumulate home equity more rapidly, thus increasing your ability to cover large emergency expenditures.

- Choose home repair contractors wisely. Favor contractors who have successfully performed work for people you know. Insist on a written, fixed-price bid. Don't make full payment until satisfactory completion of the work.

- Ask your local electric or gas utility for a free or low-cost home energy audit. The audit may reveal inexpensive ways to reduce home heating and cooling costs by hundreds of dollars a year. Keep in mind that a payback period of less than three years, or even five years, usually will save you lots of money in the long-term.

- Weatherproof your home. Caulk holes and cracks that let warm air escape in the winter and cold air escape in the summer. Your local hardware store has materials, and quite possibly useful advice, about inexpensively stopping unwanted heat or cooling loss.

- Use window coverings to block or let in sunshine. In summer, use these coverings to block sunlight, keeping your house cool. In winter, open the coverings to let sunshine warm the house. You could easily save more than $100 annually while being more comfortable.

- Look for sales at discount outlets. There are huge price differences between clothing on sale at discount stores and that sold regularly at many department and specialty stores, though keep in mind that prices at the latter are often deeply discounted.

- Consider purchasing previously-used clothes from Good Will, second-hand stores, or school or church thrift sales. With a little effort, you can find low-priced, high-quality used clothing items that can be worn for many years.

- Assess clothing in terms of quality as well as price. An inexpensive shirt or coat is a poor bargain if it wears out in less than a year. Consider fabric, stitching, washability, and other quality related factors in your selection of clothes.

- Clean clothes inexpensively. Wash and iron clothes yourself. If you use a cleaner, compare prices at different establishments. A 50 cent difference in cleaning a shirt, for example, can add up to $100 a year.

- Assess your communications costs. As Internet and wireless use grows, many consumers are overpaying for unneeded communications capacity. For example, if you have a cell phone and two phone lines -- one for your computer -- consider receiving personal calls on your cell phone so you can give up one of the phone lines.

- Communicate by e-mail rather than by phone. If you're on-line, e-mail communications are virtually free.

- Be aware of your cell phone costs and how to reduce them. Cell phone use has dramatically increased communications expenditures in many households. Understand peak calling periods, area coverage, roaming, and termination charges. Make sure your calling plan matches the pattern of calls you typically make.

- Research free or inexpensive entertainment in your community. Use local newspapers and websites to learn about free or low-cost parks, museums, film showings, sports events, and other places which you and your family would enjoy.

- Give up premium cable channels or better yet, cable altogether. It's a lot cheaper to rent one film a week than watch one on premium cable channels that may cost more than $500 a year.

- Borrow books rather than purchasing them. Borrowing books and reading magazines at your local library, rather than purchasing reading material, can save you hundreds of dollars a year.

- Attend high school rather than college or pro sports events. High school sports events rarely cost more than $5 and are often free, with hot dogs and sodas typically costing $1-2. College and pro football and basketball games rarely cost less than $20, and their concessions are usually several times more expensive.

- Plan gift-giving well in advance. That will give you time to decide on the most thoughtful gifts, which usually are not the most expensive ones. And if these gifts are products that must be purchased, you will have the opportunity to look for sales.

- In families, discuss limits on spending for gifts. These limits not only tend to reduce expenditures; they also be greatly appreciated by the least affluent family members.

- Socialize at pot-luck meals rather than at restaurants. Because one wants to be generous to friends and family, there may be huge cost savings here.

- Consider writing letters instead of making frequent phone calls. Thoughtful letters are usually far more highly valued than phone conversations, and they are often saved by recipients for future reading.

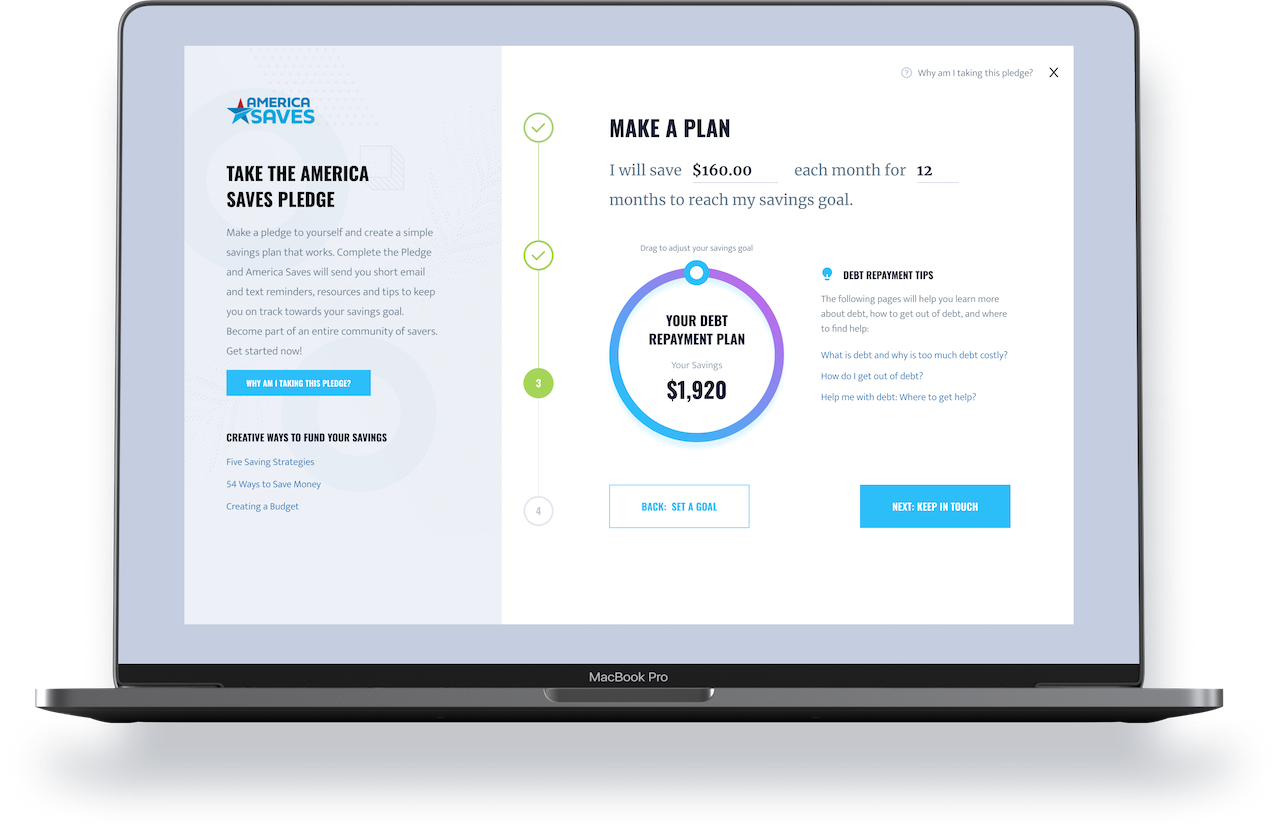

Take the Military Saves Pledge

Want inspiration and motivation on your savings journey? Take the Military Saves Pledge today and create a simple personal savings plan that works!

Take the Veteran Saves Pledge

Make a pledge to yourself and create a simple savings plan that works. Complete the Pledge and Veteran Saves will send you short email and text reminders, resources, and tips to keep you on track toward your savings goal. Become part of an entire community of savers. Get started now! Please use a CIVILIAN email address.

Creative ways to fund your savings

Those with a savings plan are twice as likely to save successfully. Taking the Veteran Saves Pledge is a pledge to yourself to start a savings journey and Veteran Saves is here to encourage you along the way. Take the first step toward creating a better financial future. Make a plan, set a goal, and pledge to yourself to start saving, today.

Congrats on completing the pledge!

We are so glad you have started your savings journey and Veteran Saves will be right beside you the whole way! You will soon receive an email from the America Saves team to help encourage you. Find helpful links below to continue researching topics on saving.

General - Save Automatically

#Save automatically using an allotment with #myPay to automatically transfer funds monthly into a #savings account http://ow.ly/sGWxb

Check out savings journeys from savers just like you

When You Start Small, Saving is Easy

08.12.2019

When Attiyya first got married, she and her Marine husband had just graduated from college and were focused on paying off student loan debt. They had both attended private schools and had sizeable loans. Then three months after the wedding, the couple found out they were pregnant with their first child.

Setting a Goal Leads to Success

05.24.2019

Growing up, Marisa’s dad had always talked about saving first, but she said she didn’t really internalize...

From Shopaholic to Saver

01.13.2021

Many of us spend too much money on things we don’t need, but we don’t always know why. It’s easy to get a...

Making Saving Automatic Leads to Personal Success

05.27.2020

Ryan’s savings journey started when he was an active duty airman. Frequent deployments and temporary duty...

Building a Six-Figure Savings While Enjoying Life

11.13.2020

Does the idea of saving up hundreds of thousands of dollars seem impossible? How about doing it while sti...

or

If we feature you in our newsletter, you get $50.